The Cheapest Trillion-Dollar Stock in the World

Riccardo Alberti

A 20Quant Saturday Brief on Micron, the HBM supply chain, AI infrastructure, the latest Turbulence Index regime, and the key market events to monitor in the week ahead.

01 — The Memory Cycle Meets AI Infrastructure

The cheapest trillion-dollar stock in the world

Micron is worth a trillion dollars now, which sounds like a lot until you look at what the market is paying for it. Sixteen times earnings for the fiscal year ending this August. Nine times the one after. Numbers one would expect from a chemicals company in a decent year, not from a name now treated as core AI infrastructure.

The market has not made up its mind about what memory has become. HBM lives inside AI servers, customers plan around it months in advance, supply is tight and capacity gets locked up in agreements that look nothing like the old spot-market scramble. The market accepts that part. It has not accepted the next one: memory may no longer be the same cycle.

Saying memory is now infrastructure means rerating the sector, not just revising next quarter’s numbers. By the time the evidence arrives, the price has usually done part of the work.

So Micron sits in an unusual place. If the HBM dynamic is real and durable, the multiple looks too low. If supply loosens or AI capex cools, the same multiple suddenly looks generous. Micron now trades on a very specific question: how much of the old memory cycle is still left in the business?

02 — Stocks of the Week

Micron Technology and the HBM supply chain

The exposure this week is Micron.

Plenty of names go up when AI sentiment is good. Micron is the one that forces an actual decision about whether the memory business has changed shape.

The bull case is no secret. AI servers eat memory, HBM is constrained, customers are booking capacity earlier than they ever have, visibility is unusually clean.

The problem is that the stock has already absorbed most of it. The price has run roughly 30% past the average analyst target in the material we reviewed, and consensus has been raising numbers into a move rather than ahead of one.

A supply normalisation, a softer AI capex cycle, a Samsung ramp that lands a quarter earlier than expected: any of those takes the multiple apart fast.

The next test is the FQ3 print in late June, when the market gets a cleaner look at HBM revenue at scale.

And the broader basket

Around Micron we look at SK Hynix as the closest listed peer in high-bandwidth memory.

Applied Materials is the equipment leg: larger, deeper, lower beta, but already valued as a premium beneficiary of the capacity buildout.

Entegris, which supplies advanced materials and process chemicals, sits closer to the materials and packaging bottleneck, with more idiosyncratic risk and less liquidity.

SMH is the broader semiconductor wrapper, already up strongly this year, for exposure that does not depend entirely on one memory name.

The next earnings beat matters less than the moving parts behind it: HBM pricing, Samsung’s ramp, Chinese competition and how crowded the semiconductor trade becomes before investors start taking profits.

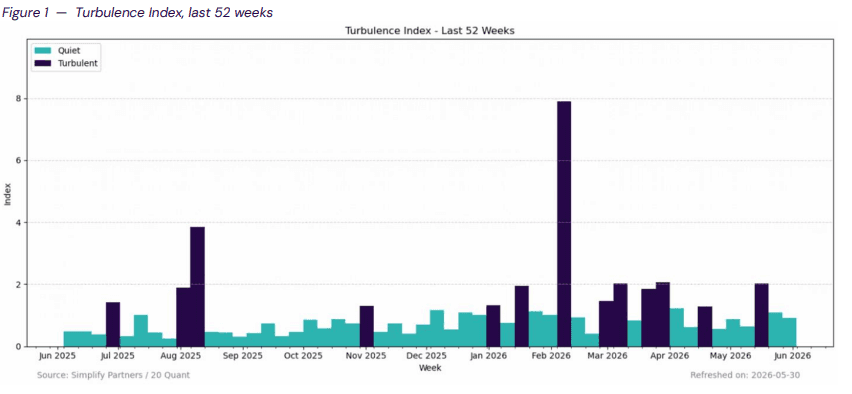

03 — Turbulence Index

Measuring stress beneath the surface

Before turning to this week's signal, a brief note on what the Turbulence Index measures.

The Turbulence Index is not a volatility gauge, and it is not designed to predict the next move in the S&P 500. It is a cross-asset stress indicator.

It measures whether market structure remains orderly, or whether correlations and linkages between assets are starting to drift away from their normal behaviour.

Stress does not always surface immediately in the main equity indices. Sometimes the indices stay resilient while fragility, dislocations and tensions between assets build beneath the surface.

Current regime: Quiet

The Turbulence Index remained quiet this week. Cross-asset linkages continue to look more stable after the stress reading in the week of 16 May, while the S&P 500 advanced by about 1.4% over the week.

The reading fits the week’s market tape: equities moved higher, while cross-asset relationships stayed orderly.

A quiet regime does not remove risk. It says the structure is cleaner. Correlations are behaving in a more orderly way, and historically this has been a better backdrop for risk-adjusted equity outcomes than turbulent periods.

For this week’s Brief, the point is straightforward. Micron and the HBM basket are not fighting a hostile cross-asset regime, but the trade remains exposed to semiconductor crowding, AI capex expectations and any repricing in rates.

What this means for the theme

A Quiet regime is consistent with a more constructive posture toward risk. For the Micron theme, that means the cross-asset backdrop is not adding pressure to the position.

The trade's internal risks, HBM crowding, AI capex expectations, semiconductor positioning, remain live and are not hedged by the regime reading itself.

04 — Wrap-Up: Next Week

What to watch next week

With the Turbulence Index Quiet again, three things matter going into next week: the composition of US payrolls, what a sticky Euro print does to the currency, and whether the AI infrastructure trade can absorb two stress tests in five days.

Payrolls: composition, not headline

The headline number will get the screen time. The composition tells a different story, and has been telling it for two months. Financial services and information have led job losses since March.

If that holds again, the market gets confirmation that the slowdown is concentrated in the high-wage, rate-sensitive part of the economy, which is exactly what the bond market has been quietly pricing through curve steepening.

A strong headline with weak internals is not a print that supports rates. It supports duration. We watch the diffusion index more than the top line.

Market relevance: Treasuries, the dollar, rate-sensitive equities, credit spreads, financials, information technology, rates volatility.

Euro CPI: the currency, not the policy

Consensus expects 2.9% year-on-year, after 3.0% in April. The temptation is to read a sticky print as a rate story, but the ECB has already signalled it will not be rushed.

The real channel is the euro, which has been strengthening for six weeks while no one was looking. Another sticky print extends that move, and the European corporates most exposed to a stronger EUR are the same names that have been carrying the Stoxx 600: luxury, autos, capital goods.

A 2.9% print does not change the June 10-11 meeting. It changes the FX backdrop for European exporters.

Market relevance: EUR/USD, Bunds, EUR rates, European exporters, European banks, utilities, real estate, investment-grade credit.

Broadcom and SpaceX: two stress tests for the AI premium

Both events test the same question this Brief opened with. Where does AI infrastructure deserve a premium, and where has the price already moved too far?

Broadcom is the cleanest read on whether custom silicon is becoming a real alternative to NVIDIA, or whether it remains a niche story dressed up in macro language.

The number to watch is AI revenue guidance, not the headline beat. If guidance accelerates, the breadth of the AI infrastructure trade widens and the Micron read-across is positive. If it disappoints, the trade narrows back to the usual three or four names.

SpaceX is a different test. According to Bloomberg, the company is reportedly targeting a $75bn raise at a valuation above $2tn for a loss-making business.

That is the market openly asking how much it is willing to pay for AI-adjacent infrastructure that does not yet make money. The reception of the roadshow tells you more about positioning and risk appetite than any sell-side survey.

Market relevance: semiconductors, AI networking, custom silicon names, private-market valuations, space-related equities, Nasdaq risk appetite, passive flows.

05 — Closing

In brief

One number to remember: Micron at 9x FY2027 earnings. AI infrastructure demand is being priced into the stock, while the valuation still carries the memory-cycle discount.

That gap holds only if HBM keeps supply tight, pricing firm and customer commitments longer than in previous cycles. If those assumptions weaken, the old memory cycle comes back quickly.

Next week brings the tests around it: jobs for rates, Euro CPI for policy, Broadcom and SpaceX for the AI infrastructure trade.

Market Insights

Selected research notes on macro regimes, risk dynamics, and portfolio implications across market cycles.