The Google $85 Billion Question

Riccardo Alberti

A 20Quant Saturday Brief on Alphabet’s $84.75 billion equity raise, the financing of the AI infrastructure cycle, the latest Turbulence Index regime, and the key market events to monitor in the week ahead.

01 — The Google $85 Billion Question

The Equity Machine

Alphabet raised $84.75 billion this week. The figure alone would be remarkable, but the identity of the issuer is what makes it a market event. Alphabet is not a start-up hunting for survival capital. It runs a dominant search franchise, a cloud platform still scaling, and a balance sheet most CFOs would envy. When a company of that profile turns to the equity market for that amount, the deal stops being about Alphabet and starts being about how the AI cycle gets paid for.

The structure carries the message. Common stock, mandatory convertible preferred, a $10 billion private placement to Berkshire Hathaway, a further $40 billion through an at-the-market programme starting in the third quarter. Read together they look less like a one-off raise and more like a template for the rest of the hyperscaler complex.

The arithmetic explains the urgency. 2026 capex is tracking around $186.6 billion against consensus free cash flow closer to $22 billion. That gap is too large to be closed by retained earnings, even at this scale, which is why the equity market is now being asked to fill it. At today's price the earnings yield sits below the US 10-year Treasury through 2027 on GAAP estimates, and the equity risk premium only turns positive in 2028, conditional on the expected earnings acceleration arriving.

Alphabet now trades on a very specific question: whether the cash flows from this buildout arrive on a schedule that justifies the equity being issued to fund them.

02 — Stocks of the Week

Alphabet and the AI infrastructure chain

The exposure this week is Alphabet.

The stock matters because it turns the AI trade into a balance sheet question. Alphabet has moved from beneficiary of AI demand to one of the companies being asked to finance the physical layer behind it, and the equity raise is the moment that becomes visible on the cap table.

The bull case is no secret. AI capex is being deployed early, the company has the operating engine to absorb it, the Berkshire placement gives the raise a visible reference point, and the mandatory convertible widens the institutional buyer base. If Google Cloud, Gemini and enterprise monetisation deliver, the dilution will be remembered as the cost of securing capacity ahead of the field.

The problem is that the ATM programme creates a disclosed supply overhang from the third quarter, capex guidance is still moving up, and the earnings yield stays below the US 10-year Treasury through 2027 on GAAP estimates. The market is funding infrastructure today for earnings that still have to arrive.

The next test sits outside the stock itself: if Microsoft, Meta or Amazon arrives with a similar structure inside two quarters, this stops being an Alphabet event and becomes a sector template.

And the broader basket

Around Alphabet, Microsoft is the cleanest peer read, with a smaller funding gap and stronger free cash flow coverage that make its next capex update the most important comparison in the sector.

Nvidia is the capex destination, since most of the hyperscaler AI budget still flows into compute and networking, although the stock already carries a heavy load of AI optimism and the read-across is less asymmetric than it was a year ago.

Corning, Vertiv and Eaton give exposure to the physical layer the spend is built on: optical connectivity, thermal management, and electrical and grid equipment respectively. All three have rerated meaningfully on the same thesis, so the open question is whether order books and margins can keep up with the multiples.

IGV is the wrapper for the monetisation side, where the test is whether the capex eventually becomes software revenue rather than stranded capacity.

The basket is built around funding mechanics rather than AI enthusiasm. What matters next is whether a second hyperscaler validates the equity-financing template Alphabet has just put on the table.

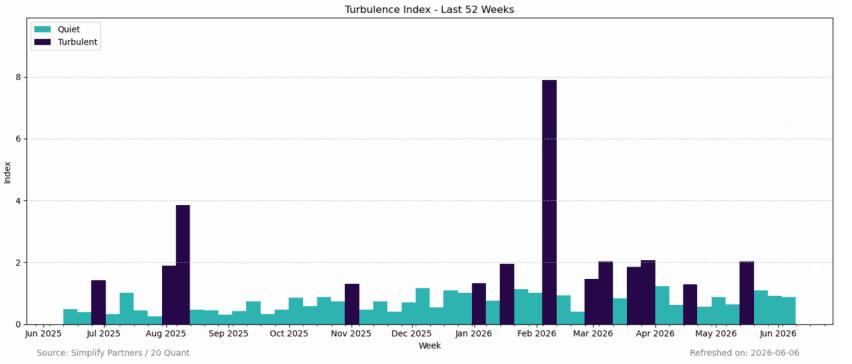

03 — Turbulence Index

Measuring stress beneath the surface

Before turning to this week's signal, a brief note on what the Turbulence Index measures.

The Turbulence Index is not a volatility gauge, and it is not designed to predict the next move in the S&P 500. It is a cross-asset stress indicator. It measures whether market structure remains orderly, or whether correlations and linkages between assets are starting to drift away from their normal behaviour.

Stress does not always surface immediately in the main equity indices. Sometimes the indices stay resilient while fragility, dislocations and tensions between assets build beneath the surface.

Current regime: Quiet

The Turbulence Index stays in Quiet for the third consecutive week. Cross-asset linkages continue to behave in a more stable way than during the stress period around mid-May.

A Quiet regime does not remove risk. It says the structure is cleaner. Correlations are behaving in a more orderly way, and historically this has been a more supportive backdrop for risk-adjusted equity outcomes than turbulent periods.

What this means for the theme

A third consecutive Quiet reading matters more for the Alphabet trade than it would for a defensive position. The capex thesis this Brief opened with is long duration and crowded, which makes it more vulnerable than most to a sudden cross-asset stress event.

The Turbulence Index says that risk is not currently building. The trade's specific risks, the ATM supply overhang, capex versus monetisation, hyperscaler positioning, remain live and are not hedged by the regime reading itself.

04 — Wrap-Up: Next Week

What to watch next week

Four events test the question Alphabet's raise opened this week: whether the market will keep funding AI earnings before the earnings actually show up. Apple's developer conference, US CPI, Oracle earnings and the ECB decision each push on a different part of the answer.

Apple WWDC: the user layer

Apple's Worldwide Developers Conference starts Monday and the market will watch Siri. The real issue is whether Apple can turn AI into something that changes usage, upgrades and services revenue, which is what makes WWDC the cleanest contrast to Alphabet's infrastructure story.

A credible Siri reset, especially one that opens the device to external AI agents, broadens the AI trade beyond GPUs, cloud and data centres and gives the market a reason to price consumer distribution again.

If the event disappoints, the trade stays concentrated in the names that control compute and cloud capacity, which keeps the pressure on Alphabet to convert spending into revenue before investors lose patience with the capital intensity.

Market relevance: Apple, Nasdaq leadership, App Store economics, consumer technology, AI software platforms, mega-cap breadth, semiconductors.

US CPI: the rate test for the AI multiple

Alphabet's raise only works if investors stay willing to pay now for earnings expected later, and that willingness runs through rates. A softer print gives the long-duration trade more room to accept a low current earnings yield in exchange for the 2027 and 2028 payoff.

A sticky print keeps the risk-free rate high and lifts the hurdle for every company asking the market to finance future earnings. Composition matters more than the headline. Services, shelter and transportation will tell investors whether inflation is genuinely cooling or simply rotating through the basket, and for AI infrastructure stocks that distinction is the difference between a tolerable and a tightening backdrop.

Market relevance: Treasuries, real yields, Nasdaq, mega-cap technology, growth equities, credit spreads, rate volatility, US dollar.

Oracle: the next infrastructure check

Oracle reports after the close on Wednesday. The cloud infrastructure line has been growing at an unusually high pace, and the market will care more about forward guidance than the headline beat.

The question is whether Oracle can bring additional GPU capacity online and convert demand into revenue fast enough to support the next leg of estimates. A strong print supports the Alphabet thesis by suggesting the capex cycle is broadening rather than concentrating in two or three names.

A weak one sharpens the concern that capex is running ahead of monetisation, which is precisely the imbalance Alphabet's equity raise has put on the table.

Market relevance: Oracle, cloud infrastructure, hyperscalers, AI servers, Nvidia, Broadcom, data-centre suppliers, Nasdaq risk appetite.

ECB: the global duration channel

The ECB decision is not the centre of this Brief, but it belongs in the week ahead because of duration. Alphabet's valuation is also a rates story, and so is the broader AI infrastructure basket.

A hawkish path runs through Bunds, the euro and global financial conditions, and while it does not change Alphabet's strategy, it can change the market's tolerance for long-duration equity risk.

A stronger euro adds an FX layer for European exporters, and higher European yields keep pressure on rate-sensitive sectors. The read-across to US technology is second order but no longer trivial: global duration has stopped being a US Treasury story alone.

Market relevance: EUR/USD, Bunds, global duration, European equities, banks, utilities, real estate, US growth equities, credit spreads.

05 — Closing

In brief

One number to anchor the week: Alphabet at an earnings yield below the US 10-year Treasury through 2027. The market is being asked to pay now for earnings that still have to arrive, and the equity raise has put the gap on the table in the cleanest possible form.

The Turbulence Index in Quiet for a third consecutive week says the cross-asset structure is not adding pressure to the trade. The risks that matter sit inside the trade itself: ATM supply, capex versus monetisation, hyperscaler crowding.

This raise is a marker for the hyperscaler complex, and we would not be long the basket into the ATM window without watching how Alphabet's supply trades over the next six to eight weeks.

The view changes on two signals: Oracle's print on Wednesday, which tests whether infrastructure demand is broadening, and any sign that Microsoft, Meta or Amazon are preparing similar structures. A second hyperscaler issuance turns this from an Alphabet event into a sector repricing.

Next week brings the tests around it: Apple for the consumer layer, US CPI for the rate test, Oracle for the infrastructure read, and the ECB for global duration.

Market Insights

Selected research notes on macro regimes, risk dynamics, and portfolio implications across market cycles.