World Cup 2026: What Is Already Priced in?

Riccardo Alberti

This Saturday Brief examines the 2026 World Cup as a stock-specific market catalyst, with Booking Holdings as the preferred exposure, a Turbulent regime signal from the 20Quant Turbulence Index, and the key macro events to monitor next week.

Executive Summary

World Cup 2026

The tournament will generate measurable demand across travel, payments and consumer spending, but the investment opportunity is stock-specific rather than market-wide.

Booking Holdings stands out with an attractive valuation, strong quality metrics and direct exposure to travel demand.

Macro developments dominate event-specific catalysts. The 20Quant Turbulence Index has shifted from Quiet to Turbulent.

01 — 104 Matches & 16 Host Cities

What is already priced in?

The 2026 World Cup begins next week with 104 matches across sixteen host cities in the United States, Canada and Mexico. It is the largest tournament in FIFA history and will generate a meaningful increase in travel, accommodation, payments, advertising, consumption and betting activity.

For investors, however, the question is not whether demand will rise. It is whether that demand is large enough to move earnings expectations and share prices.

History suggests caution. World Cups create visible economic activity but rarely produce broad and lasting market outperformance. Most large-cap companies absorb the impact within a single quarter of earnings, while macro forces such as rates, geopolitics and consumer confidence remain the dominant drivers of valuation.

That makes stock selection more important than thematic exposure.

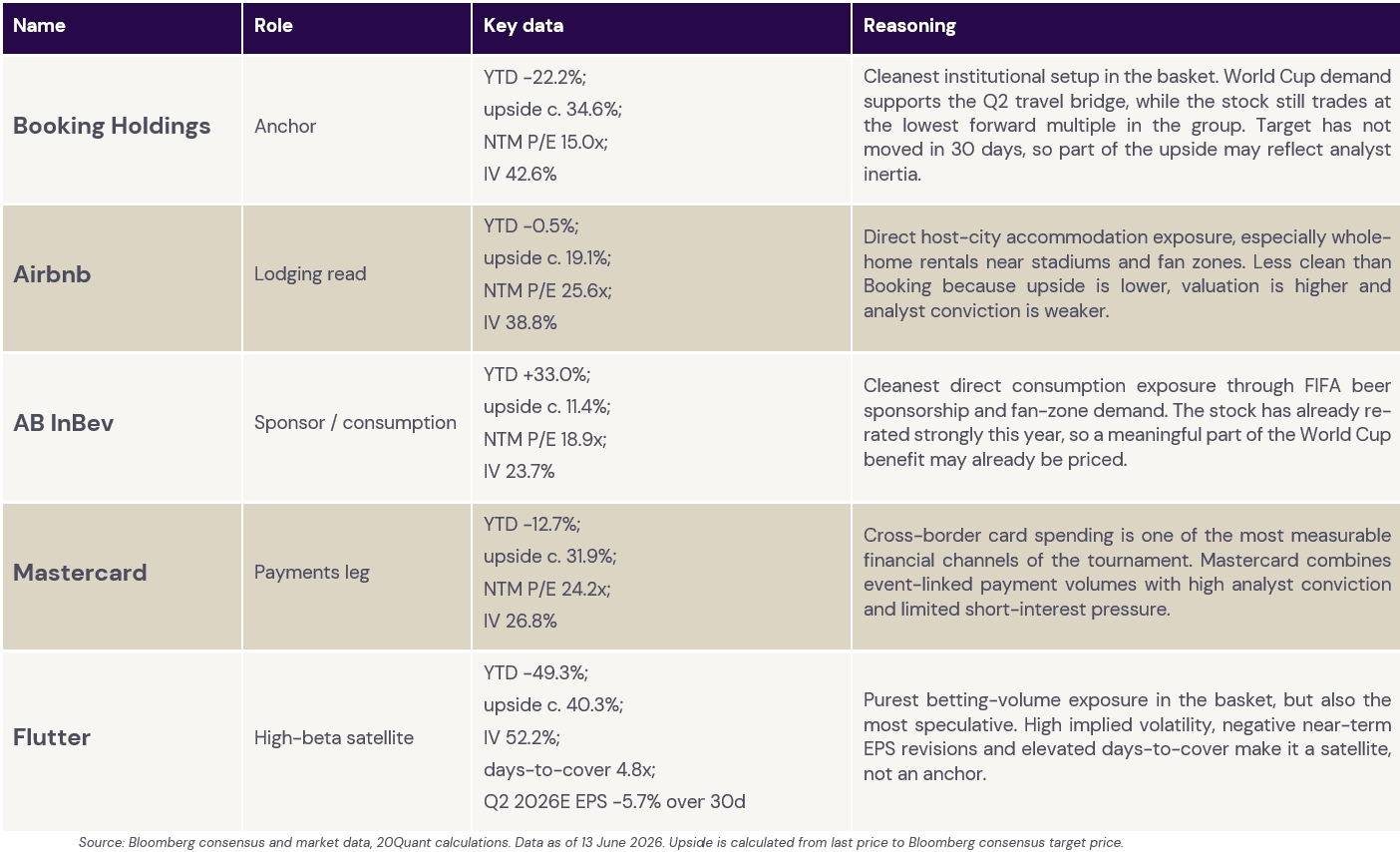

Among the most direct beneficiaries, Booking Holdings stands out. Unlike pure event-driven trades, the investment case combines a discounted valuation, strong profitability and direct exposure to travel demand. The tournament does not need to transform the business. It only needs to support booking activity at a time when investor expectations remain subdued.

Other names offer more targeted exposure. Mastercard captures cross-border spending. Airbnb benefits from accommodation demand. AB InBev remains the clearest consumption and sponsorship play. Flutter provides the strongest betting exposure but also carries the highest volatility.

The market opportunity therefore lies not in owning a generic World Cup basket, but in identifying the small number of companies where valuation, earnings sensitivity and timing align. Booking remains the clearest example of that setup.

02 — Stocks of the Week

Where the World Cup can still matter

The exposure this week is Booking Holdings.

The stock matters because it separates the World Cup theme from the World Cup headline. Booking is a travel recovery candidate where the tournament can help the numbers arrive at the right time, not a generic event play.

The factor read supports the setup. Booking scores strongly on profitability and conservative investment quality and looks attractive against its own historical valuation range. Momentum is weak, which is the entry point: the stock has been trading like a travel name under geopolitical pressure rather than like a clean event beneficiary, and that gap is what the tournament could narrow.

The bull case is that the market is too focused on travel disruption and not enough on the demand bridge ahead. If geopolitical pressure fades into the summer window, host-city accommodation demand stabilises the Q2 narrative and gives investors a reason to look through current room-night weakness.

The problem is that the same logic works in reverse. A 39-day tournament cannot offset a full-year travel shortfall if Iran-linked disruption persists into Q3. Booking is the right name only if framed honestly: valuation recovery first, World Cup catalyst second.

The next test is the Q2 call, where the theme either shows up in the numbers or disappears into macro noise.

And the broader basket

Booking remains our preferred exposure within the World Cup basket.

Airbnb offers the most direct accommodation exposure, but trades on a meaningfully higher valuation and leaves less room for multiple expansion.

AB InBev provides the clearest sponsorship and consumption link, although the stock has already re-rated strongly this year.

Mastercard benefits from cross-border spending flows but remains more exposed to the broader travel cycle than to the tournament itself.

Flutter is the highest-beta expression of the theme. Betting volumes should benefit directly from the tournament, but elevated implied volatility, weaker earnings revisions and higher execution risk make it better suited as a satellite position than a core holding.

The key distinction is between exposure and opportunity. Many companies will benefit from World Cup-related activity, but only a few combine earnings sensitivity with attractive valuation. On that basis, Booking continues to offer the most compelling balance of valuation, quality and catalyst support heading into Q2 earnings.

03 — Turbulence Index

Measuring stress beneath the surface

The Turbulence Index is a cross-asset stress indicator. Rather than forecasting the next move in equities, it measures whether relationships between assets remain orderly or begin to diverge from historical patterns.

Market stress does not always appear first in headline indices. It often emerges through changing correlations and dislocations across asset classes before becoming visible in equity performance.

Current regime: Turbulent

The Turbulence Index has moved back into Turbulent territory after three consecutive Quiet readings. Cross-asset relationships have become less stable, suggesting a less supportive backdrop for risk assets.

A Turbulent reading does not imply an imminent market decline. It does, however, indicate that macro drivers are becoming more influential and that headline equity resilience may provide an incomplete picture of underlying market conditions.

What this means for the theme

The regime shift raises the hurdle for event-driven trades. World Cup-related catalysts may still support individual stocks, but they now compete with a macro environment increasingly driven by geopolitics, rates and cross-asset stress.

As a result, the investment case depends more heavily on early evidence of earnings impact than it would in a more stable market regime.

04 — Wrap-Up: Next Week

What to watch next week

The World Cup begins against a busy macro backdrop. The key question is whether event-driven catalysts can gain traction before geopolitics, central bank policy and corporate spending reassert themselves as the dominant market drivers.

G7: the geopolitical filter

The G7 summit starts Monday and remains the most important geopolitical event of the week. For travel-related names such as Booking, Airbnb and Mastercard, easing tensions would support the travel recovery narrative.

Escalation would likely have the opposite effect, with macro concerns overwhelming tournament-related demand.

Fed, BOJ, BOE: the rate and FX filter

Three major central banks meet next week. The Fed remains the most important for equity valuation, while the BOJ and BOE will influence currency markets, rates expectations and broader risk sentiment.

Accenture: the corporate spending check

Accenture reports on Thursday and may prove more important for markets than any single World Cup data point. The company sits at the intersection of enterprise technology spending, AI implementation, cloud adoption and consulting demand.

A strong result would reinforce the view that corporate investment remains resilient despite macro uncertainty. A weak result could raise concerns about technology spending, digital advertising and broader risk appetite, with implications extending well beyond the company itself.

05 — Closing

In brief

The World Cup begins next week, but the broader market backdrop remains the dominant driver of risk. The 20Quant Turbulence Index has moved back into Turbulent territory, suggesting a less supportive environment for event-driven trades.

Booking remains our preferred exposure within the World Cup basket, combining attractive valuation, strong quality metrics and direct sensitivity to travel demand. However, the investment case depends as much on macro conditions as on the tournament itself.

Three developments matter most next week: the G7 summit, central bank meetings and Accenture’s earnings. While early World Cup demand data will provide an initial test of the theme, Accenture may prove the more important signal, offering insight into corporate spending, AI investment and broader risk appetite.

The key question is whether tournament-related demand can support earnings expectations before geopolitics, rates and macro uncertainty regain control of the narrative.

Market Insights

Selected research notes on macro regimes, risk dynamics, and portfolio implications across market cycles.